It is difficult to increase the start of downstream products enterprises. With the impact of temperature drop and transportation, the demand has basically ended, and the demand in North China has gradually become bearish in the later period, and the upward pressure on PVC is still relatively large. It is expected that the domestic PVC market will remain weak in the short term.

The current public health event is a double-edged sword, with the impact gradually spreading from upstream to downstream. From the downstream point of view, the improvement in demand is not obvious. Although the current export has improved slightly, it is far from the first half of the year. In the middle and late quarter of the fourth quarter, PVC is still oversupplied, but in November, the supply and demand may be relatively balanced due to the maintenance of downstream demand and the increase of upstream production reduction.

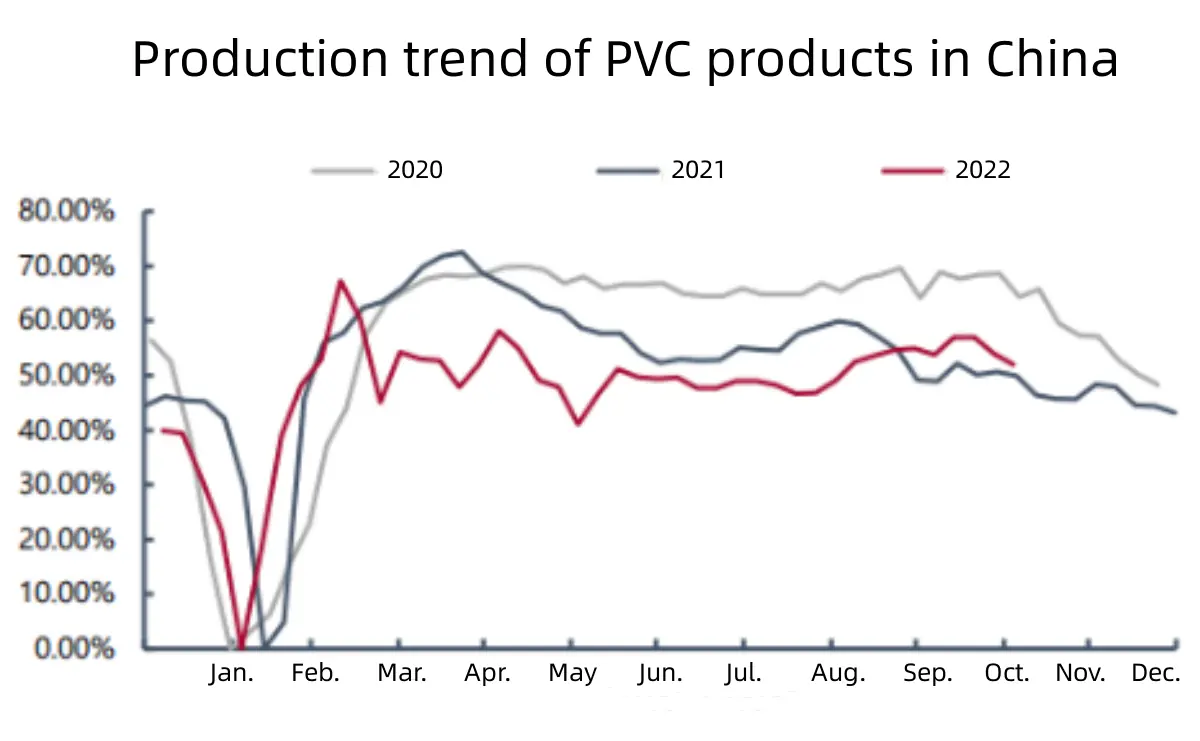

① In the short term, the start-up of PVC enterprises continues to remain low, the supply is reduced but the demand has not increased

Although the price of raw material calcium carbide is loose, the cost pressure of PVC enterprises is still relatively large, and it is difficult to increase the start of construction in the short term, and the supply is tight. In the fourth quarter of domestic PVC and the first quarter of 2023, supply and demand pressure may be greater.

②The autumn inspection is over, the traditional peak season is over, and new production capacity will be launched, which will exacerbate the imbalance between supply and demand

The Spring Festival this year is earlier, and the demand vacuum period may appear earlier, and the main idea is bearish. From a long-term perspective, it may still be a pattern of low volatility. In the next one or two years, due to the goal of carbon peaking, the domestic production capacity of some high-energy-consuming industries may be cleared, but PVC is still a passive follower, and the cycle of eliminating production capacity may be longer than other black series.

③ The start-up of PVC product enterprises has not changed much, and the original load is mainly maintained.

From the perspective of profile companies, Xinjiang is basically in a state of shutdown, and other regions have local transportation controls, and the overall operation is flat. From the perspective of the overall industry, the policy has limited boost to domestic demand, the downstream industries are still limited by the terminal, orders are tepid, and the demand in the north continues to be bearish after November. According to information research, in terms of raw materials for profile enterprises, some orders at low prices are the mainstream this week, and large-scale orders are the mainstream in the long run, and the inventory cycle ranges from 15-25 days. In terms of product inventory: maintaining a medium-to-upper position, the pressure on partial shipments is still there. In terms of start-up: 4-60% of the start-up load will be maintained, and order delivery will be the mainstay.

In short, the domestic PVC market maintains a weak trend of supply and demand. On the supply side, there are many production cuts and parking lots. Although the inventory of the two warehouses has decreased month-on-month, it is still much higher than the level of the same period last year, and there is no shortage of stock in the market. On the demand side, it is difficult for downstream product companies to start construction. With the impact of temperature drop and transportation, the demand has basically ended, and the demand in North China has gradually become bearish in the later period, and the upward pressure on PVC is still relatively large. It is expected that the domestic PVC market will remain weak in the short term.

Inspected Vinyl Floor Delivery to Kuwait | HAODIBAN

Inspected Vinyl Floor Delivery to Kuwait | HAODIBAN

Complete DIY Guide for LVP Flooring Repair

Complete DIY Guide for LVP Flooring Repair

HAODIBAN Demonstrates Reliable Delivery Capabilities

HAODIBAN Demonstrates Reliable Delivery Capabilities

New Product Recommendation: Bamboo Charcoal Wall Panels

New Product Recommendation: Bamboo Charcoal Wall Panels