FAt present, the fundamentals of domestic PVC are still weak, and the pressure of high inventory is high, and it is still necessary to wait for the further recovery of downstream demand. In the short term, under the long-short game, the PVC market is temporarily consolidating.

Recently, the trend of the domestic PVC market is still weak. Although the logistics has returned to normal and the downstream construction is also improving, overall, the PVC inventory is still at a high level. The current fundamentals are still weak, and the price of PVC has rebounded.

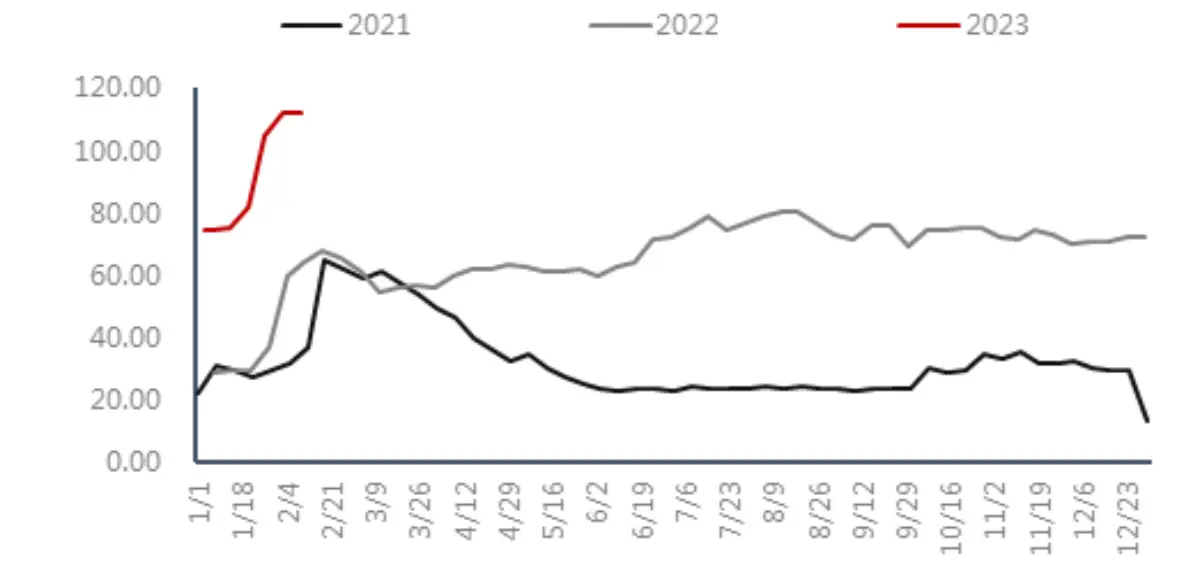

On the supply side, the current domestic PVC supply continues to maintain a high level, and the integrated enterprises have a relatively high start-up load, but the start-up load of marginal enterprises using the calcium carbide method is still relatively low. As can be seen from the above figure, the current output is lower than the year-on-year level in 2021. The main reason is that marginal enterprises are still in a state of loss, and the load is difficult to increase, but the current output has exceeded the level of the same period in 2022, an increase of 1.35% year-on-year.

From the perspective of inventory, the current inventory of PVC in the two warehouses is much higher than the same period in the previous two years. According to the statistics, the current inventory in the two warehouses has increased by 69.84% year-on-year. Mainly affected by the slow recovery of downstream demand, the current downstream product orders are not good, and most enterprises have stocked raw materials before the year, so they are currently waiting and watching. Under the pattern of price cuts and destocking, the enthusiasm for downstream procurement is not high, and the petrochemical inventory level is still at a high level.

Inventory of 48 PVC manufacturers + social inventory

On the demand side, in terms of domestic demand, the current start-up of PVC products enterprises is gradually increasing, and the start-up of soft products is better than that of hard products. From the perspective of domestic PVC profile enterprises, the overall start-up load is not high, and its terminal orders have a significant impact. In terms of raw materials for profile companies, the inventory cycle ranges from 10 to 35 days. Due to the lock-in order receiving mode, there is no obvious intention to replenish the warehouse for the time being, and they are mostly waiting for terminal orders. In terms of product inventory: the inventory cycle ranges from 15-28 days, and some of them are orders to be delivered. The start of work is maintained at 30-50%, and some are in a parking state. Looking at the industry as a whole, the market has certain expectations for after March, but there is no obvious improvement currently.

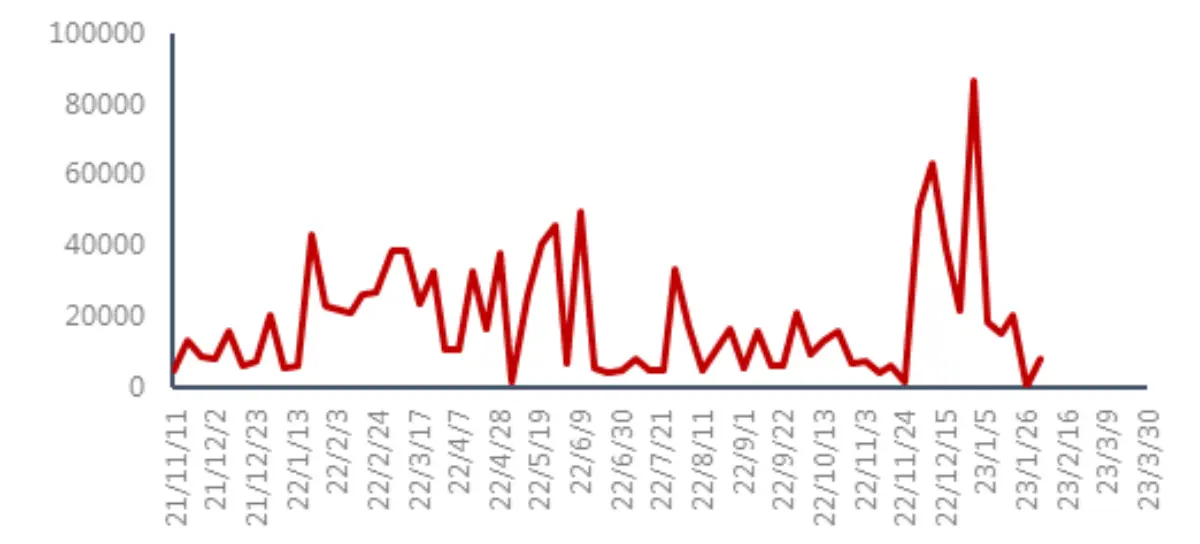

In terms of external demand: the export situation of domestic enterprises has gradually resumed. Since the peak season in India and Southeast Asia lasts until June, the current export market demand is good. However, due to the low price in the domestic market, some foreign buyers have a wait-and-see mentality.

Export signing volume of PVC production enterprises

On the whole, the current domestic PVC fundamentals are still weak, with high inventory pressure, and it is still necessary to wait for the further recovery of downstream demand. In the short term, under the long-short game, the PVC market is temporarily consolidating.

Inspected Vinyl Floor Delivery to Kuwait | HAODIBAN

Inspected Vinyl Floor Delivery to Kuwait | HAODIBAN

Complete DIY Guide for LVP Flooring Repair

Complete DIY Guide for LVP Flooring Repair

HAODIBAN Demonstrates Reliable Delivery Capabilities

HAODIBAN Demonstrates Reliable Delivery Capabilities

New Product Recommendation: Bamboo Charcoal Wall Panels

New Product Recommendation: Bamboo Charcoal Wall Panels